Freight Under Scrutiny: Where are savings headed?

Looking at the Shanghai Containerized Freight Index (SCFI) for the past year, the graph is revealing, showing a peak of tension that reached almost $2,250/TEU in mid-2025. This surge was no accident: it was the result of a perfect storm where localized congestion at key ports and the massive diversion of routes around the Cape of Good Hope absorbed capacity all at once. However, after that stress, the market has entered a sustained downward trend to the current $1,250, a figure that provides some relief to the bottom line, but which requires careful analysis.

The primary driver of this decline is the sluggishness of global consumption. Demand has yet to recover, which has reduced pressure on cargo holds. Added to this is a structural factor: oversupply. Shipping companies are receiving a wave of new, high-capacity vessels ordered after the pandemic-induced boom. There are simply more ships than cargo. Furthermore, the gradual return to the Suez Canal is injecting even more effective capacity into the system by reducing transit times and increasing fleet turnover.

Despite this “low price” scenario, we shouldn’t be overly optimistic. Shippers haven’t gained absolute negotiating power; shipping lines still control the supply. What we do have is a much more favorable negotiation environment for renewing contracts on more competitive terms than a year ago. But beware: the shipping industry is already reacting to protect its margins.

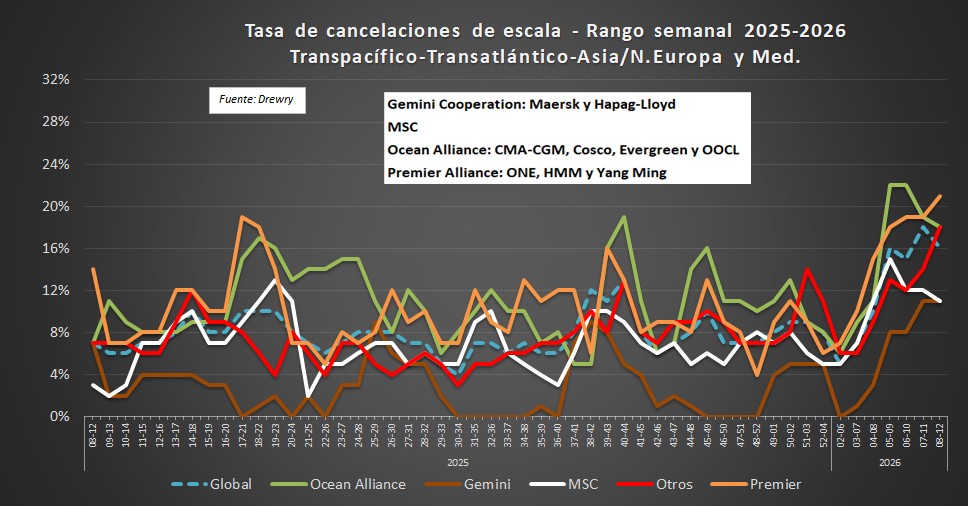

As the rate of port call cancellations shows, alliances are implementing drastic cuts to prevent a price collapse. Especially in early 2026, we see cancellation peaks exceeding 20% in the Ocean Alliance and Premier Alliance. This is the shipping lines’ defense mechanism: if there are too many ships and too little cargo, they simply stop operating port calls to artificially maintain a shortage of space.

💡 The Shipper’s Decision: Flexibility

Despite this favorable cost scenario, shippers must be alert to the potential reaction of shipping lines. With so much excess capacity, it is very likely that we will see more cancellations of port calls as they try to reduce supply and support prices.

Practical Advice: Take advantage of the current situation to negotiate, but prioritize flexibility. In a market that is still finding its bottom, now is not the time to commit to long-term contracts. Barring any geopolitical surprises, we believe that this period of calm is here to stay for a while.

Share this article

Come and visit us at Logistic & Industrial Build Madrid

Keep up to date

Freight Under Scrutiny: Where are savings headed?

Looking at the Shanghai Containerized Freight Index (SCFI) for the past year, the graph is revealing, showing a peak of tension that reached almost $2,250/TEU

Energy efficiency in the construction sector: a path towards a sustainable future

In a world where sustainability has gone from being an option to becoming an urgent necessity, the construction sector plays a decisive role. Every building,

Panattoni announces 5.000m2 lease in Panattoni Park Vitoria-Gasteiz to Kromberg & Schubert

Panattoni, a logistics-industrial real estate developer, announces the lease of two modules of the multi-tenant warehouse at Panattoni Park Vitoria-Gasteiz to Kromberg & Schubert, a

Amancio Ortega acquires two logistics centres in Germany through Pontegadea

Amancio Ortega, through his investment arm Pontegadea, has acquired two logistics centres in Germany for more than 150 million euros. This purchase is part of